Snowflake ($SNOW)

How Artificial Intelligence and Market Dynamics are Shaping Snowflake and Its Sector

Purpose of the Note: Snowflake’s recent earnings, sector performance, and how AI and sector rotation are reshaping the tech landscape. Discuss Technical Setup of SNOW.

Main Questions to answer: Was the latest earnings report, and following market reaction, enough to reset the valuation concerns and ignite a possible higher trend in price?

First, lets look at the two recent earnings releases and see what, if anything, could have led to the differences in reaction.

Comparison of Snowflake’s September and November Earnings Releases

Key Themes:

The September earnings release resulted in a sharp decline in Snowflake’s stock, while the November earnings report led to a significant 30% surge. This comparison analyzes the differences in financial results, market perception, and operational updates to identify the drivers behind the different investor reactions.

1. Financial Results Comparison

Revenue Growth:

September (Q2 FY25):

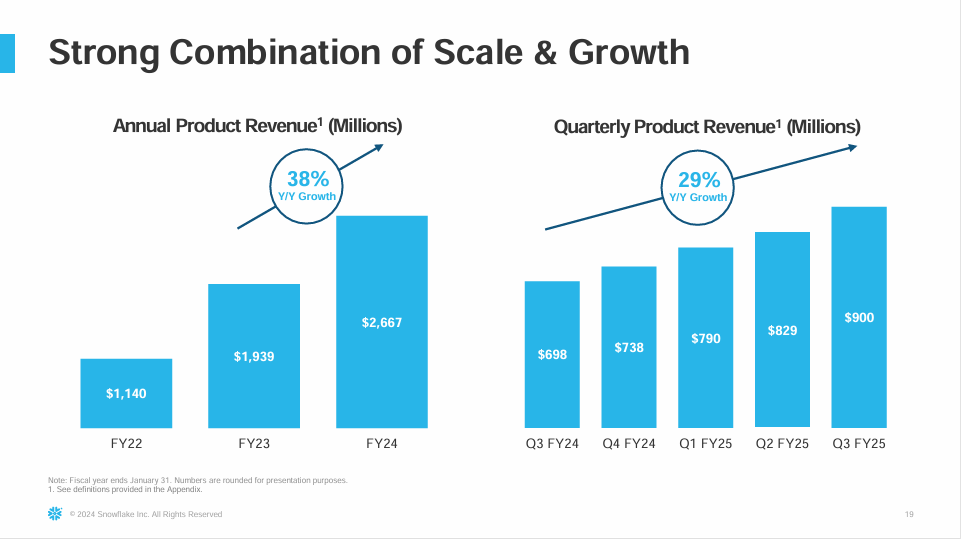

Total revenue: $868.8 million (+29% YoY).

Product revenue: $829.3 million (+30% YoY).

November (Q3 FY25):

Total revenue: $942.1 million (+28% YoY).

Product revenue: $900.3 million (+29% YoY).

Key Takeaway: Growth rates in Q3 were consistent with Q2, but the market perceived the Q2 report as signaling slowing growth momentum relative to Snowflake's historical growth trajectory.

Remaining Performance Obligations (RPO):

September: $5.2 billion (+48% YoY).

November: $5.7 billion (+55% YoY).

Key Takeaway: The acceleration in RPO growth between quarters likely restored confidence in Snowflake’s future revenue visibility and customer commitment.

Profitability and Margins:

Q2 FY25 (September):

Product gross margin: 76% (non-GAAP).

Non-GAAP operating margin: 5%.

Free cash flow margin: 7%.

Q3 FY25 (November):

Product gross margin: 76% (non-GAAP).

Non-GAAP operating margin: 6%.

Free cash flow margin: 8%.

Key Takeaway: Although margins improved slightly in Q3, the difference was marginal and likely not a decisive factor for the contrasting stock reactions.

2. Operational Metrics Comparison

High-Value Customers:

September:

510 customers with >$1 million in trailing 12-month product revenue (+28% YoY).

736 Forbes Global 2000 customers (+5% YoY).

November:

542 customers with >$1 million in trailing 12-month product revenue (+25% YoY).

754 Forbes Global 2000 customers (+8% YoY).

Key Takeaway: Growth in high-value customers remained steady, but the increase in Forbes Global 2000 customers (+8% in Q3 vs. +5% in Q2) highlighted accelerating traction among large enterprises, a key target segment for Snowflake.

3. Forward Guidance and Investor Sentiment

Q2 Guidance (September):

Product revenue for Q3 FY25: $850–$855 million (+22% YoY).

Full-year FY25 product revenue: $3.356 billion (+26% YoY).

Q3 Guidance (November):

Product revenue for Q4 FY25: $906–$911 million (+23% YoY).

Full-year FY25 product revenue: $3.43 billion (+29% YoY).

Key Takeaway: The Q3 guidance upgrade signaled optimism, exceeding the cautious tone from the Q2 release, which had highlighted slower growth rates.

4. Market and Narrative Shifts

September Report:

Stock Performance: The stock declined sharply, reflecting disappointment over slower revenue and RPO growth relative to expectations.

Narrative: Investors viewed the report as evidence of decelerating growth. Concerns over valuation in the context of a more challenging macroeconomic environment were amplified.

November Report:

Stock Performance: A 30% rally, driven by stronger RPO growth, guidance increases, and accelerating adoption of AI-driven solutions.

Narrative: The Q3 report reframed Snowflake as an AI leader, with partnerships (e.g., Anthropic) and acquisitions (Datavolo) driving growth potential. These updates aligned with market enthusiasm for AI-driven innovations, shifting sentiment from skepticism to optimism.

5. Broader Market and Sector Dynamics

September (Q2):

Market Backdrop: Investors rotated away from high-valuation tech stocks amid rising interest rates and concerns over growth sustainability.

Sector Sentiment: Skepticism dominated the software space, as other cloud companies also faced pressure on growth rates.

November (Q3):

Market Backdrop: Renewed investor enthusiasm for AI-driven narratives helped software companies regain momentum, shifting sector rotation from hardware (e.g., Nvidia) to software providers.

Sector Sentiment: Snowflake positioned itself as a clear AI enabler, leveraging its platform to address rising demand for enterprise AI solutions.

Conclusion

The contrasting market reactions to Snowflake’s September and November earnings reports stemmed from:

Revenue Visibility: Accelerated RPO growth (+55% in Q3 vs. +48% in Q2) restored confidence in future revenue streams.

Guidance: Upgraded full-year guidance in November was a sharp pivot from the cautious tone in September.

AI Narrative: Strategic updates in Q3 highlighted Snowflake’s alignment with the broader AI investment theme.

Valuation Concerns: The Q2 report raised concerns over Snowflake’s ability to sustain growth, while Q3 reaffirmed its growth potential, justifying its premium valuation.

The November earnings report capitalized on a positive shift in sentiment toward software companies with strong AI integration ( SHOP 0.00%↑ is another example) , positioning Snowflake as a key player in this rapidly evolving space.

So again, are these changes enough to change the trend?

Price Action

Outside the last week, there is not much to like on the daily or weekly charts. On the weekly, price is still stuck in this long ugly range between 200-100 or so.

However, the daily gives me some hope. On the report, we had a large gap up on heavy volume followed by three days of not great action, but on Wednesday we got one of my favorite signals, and upside reversal (purple arrow)

The questions are: did the report do enough to change the perception of the company, and is the reaction to the report enough to signal a trade?

Personally, I believe it is worth a shot.

I am starting a position with a stop below the low of the upside reversal bar. Please follow your own risk management and trade plan.

Financial Overview of Most Recent Qtr

I believe the recent quarter did enough reset the perception of the company. Therefore, I want to end with a couple slides from their most recent release.

TAM

Large and growing total addressable markets is a massive tailwind

Topline Growth

High Quality Customers

Conl:

Is SNOW about to embark on a new trend higher? Did the recent report do enough to change the company’s perception with investors? Is the price action strong enough to warrant a trade?

No one can know for sure, but time will tell.

Let me know what you think

—NS