Japan

Japan

Rising Sun, Rising Returns: Unveiling Japan's Market Potential

As a trend investor, I am always searching for investable themes. On Twitter I have been vocal about the current U.S interest rate structure and how that might lead to a prolonged period of lackluster returns for our stock market. That conclusion has lead me to at least look elsewhere for a possible positive investable theme and renewed my interest in Japan.

Today I will take a look at:

Current price structure of the Japan stock market (Nikkei 225 Stock Average)

Possible positive investment themes

Possible negative investment themes

Warren Buffett’s Japan bets and what they can mean for you

Lets Get Started !

Current price structure of the Japan stock market (Nikkei 225 Stock Average)

Going back to the 1970’s, you can see the Nikkei is still below the high made in the early 1990’s. It has made a respectable recovery after bottoming around 2009 and has been on a fairly steady uptrend since.

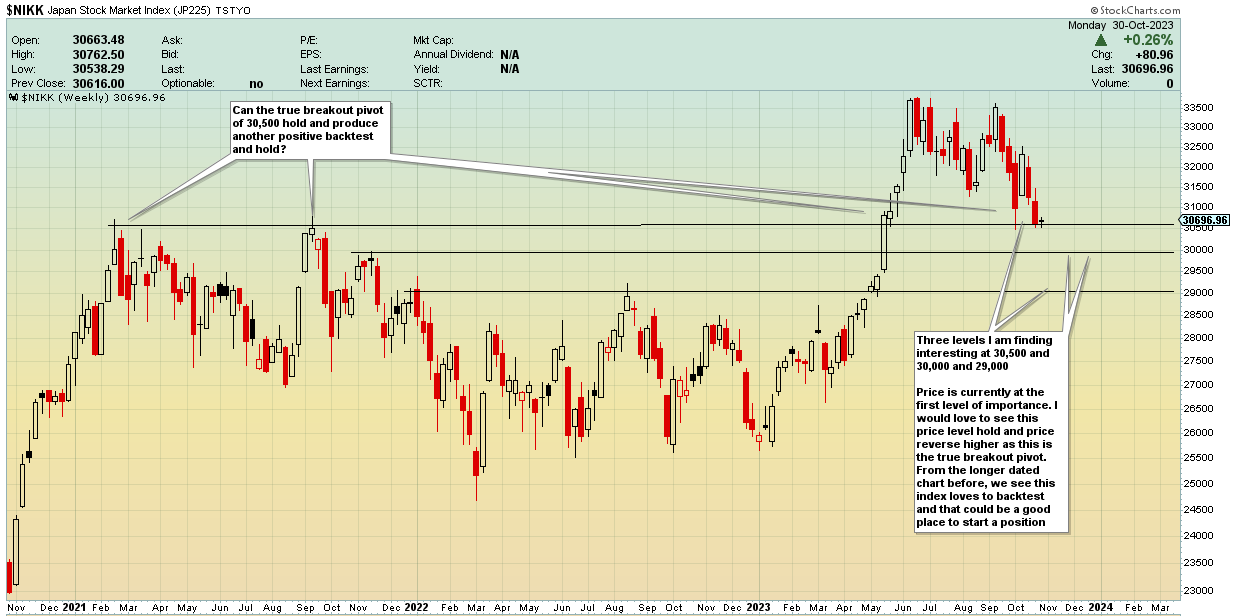

Zooming in more (weekly chart) we can see a series of higher highs and higher lows (minus the Covid crash). This indicates a long term uptrend might be in place. It also appears to have a history of breaking out, moving higher, back-testing the breakout pivot, forming a base and then moving higher again. We call this a “stairstep” pattern.

Zooming in once again (weekly chart) we can see another back test is in progress. My interest is to see IF any of the three price levels can hold. Ideally, the initial breakout pivot of 30,500 should hold. That would indicate the strongest trend and highest level of interest. But if we can get a reversal off of 30,000 or even 29,000 that could work as well for an entry.

The three levels (if the first one does not work) will be my “zone of accumulation” where I will accumulate exposure on the way down AS LONG AS price holds the final level.

Now, just looking at the daily chart above, we see price is in a daily downtrend. It is trying to find support off the 200 day simple moving average (purple’ish line) but is below the 21ema (red) and 50sma (blue) moving averages. This is not an ideal setup for a long position as the moving averages are stacked bearish. However, The longer term trend is up, and I will be looking for the price levels to hold and price to start regaining the moving averages before I even think about getting aggressive here.

Investment Tailwinds ( Positive Themes)

Households in Japan have more money to spend, which is boosting the economy. This change has caught the attention of investors like Buffett. The Japanese stock market is also becoming more appealing.

Tokyo Exchange is taking steps to address low-valued public companies, possibly delisting some by 2026. Efforts are being made to encourage companies to use their cash for share buybacks and increased dividends. This led to a record $70 billion in buybacks in 2022, with dividends predicted to reach $100 billion by 2024. Additionally, while China faces economic challenges, Japan's tech and semiconductor sectors are thriving.

Japanese companies are seeing higher profits. Corporate changes are improving management and returns. Japan's interest rates are very low compared to other countries. The Bank of Japan (BOJ) is buying assets, keeping the yield curve stable.

Fundamentally speaking:

NIKKEI's current price-to-earnings (PE) ratio is 14, lower than the S&P 500's 18.5.

The CAPE ratio is 18, which is lower than 30 for S&P 500.

The EV/EBITDA multiple is 5.25x, much lower than 13.5x for the S&P 500 as well.

The CAPE ratio (Cyclically Adjusted Price-to-Earnings) and the EV/EBITDA (Enterprise Value to Earnings Before Interest, Taxes, Depreciation, and Amortization) ratio are key valuation metrics. When these ratios are lower for one index (Japan) compared to another (S&P 500), it can suggest several attractive investment points:

Relative Undervaluation: Lower CAPE and EV/EBITDA ratios can indicate that the Japanese market, or specific stocks within it, may be undervalued relative to the S&P 500. Investors often seek undervalued markets as they offer more room for potential appreciation.

Margin of Safety: Investing in assets with a lower valuation provides a buffer or "margin of safety." If there are unforeseen negative events or market downturns, the downside risk might be lower in a market that hasn't already been bid up to higher valuations.

Less Speculation: High valuation multiples can sometimes indicate speculative bubbles or over-optimism about future earnings growth. A lower CAPE or EV/EBITDA suggests that there might be less speculative activity in the Japanese market compared to the S&P 500.

Potential for Mean Reversion: Over time, valuation ratios tend to revert to their long-term averages. If the Japanese market's valuation metrics are below their historical averages or below that of global peers, there could be potential for them to rise towards those averages, benefiting investors.

Different Growth Prospects: While valuation ratios give a snapshot of current market pricing relative to earnings, they don't capture future growth prospects. If investors believe in strong future growth for Japanese companies, the current lower ratios might seem even more attractive.

Currency Considerations: If investors anticipate that the Japanese yen might strengthen against the dollar, investments in Japan can provide currency gains in addition to any stock market returns.

Attractive Dividends: Sometimes, markets with lower valuation multiples offer higher dividend yields, providing income to investors.

Those are a brief overview of some of the possible investment tailwinds a long investor can hope to ride in the Japan stock market

However,

Nothing is all rose’s

Japanese stock market miracle more financial than real

17 August 2023

Authors: Taiki Murai and Gunther Schnabl, Leipzig University

Full artical can be found here: https://www.eastasiaforum.org/2023/08/17/japanese-stock-market-miracle-more-financial-than-real/

The above article takes the opposite standpoint. I will reword it below but you can read the article in it’s entirety by using the link.

The Japanese stock market has risen significantly since January 2023, with the Nikkei 225 index increasing by around 30%. This outperforms US and European stocks. The growth is largely due to foreign investors, with Warren Buffet's visit to Japan seen as an endorsement, and simulative practices rather then true, organic growth.

There hasn't been notable innovation in Japan's corporate sector, and financial conditions remain easy due to the Bank of Japan's (BoJ) low interest rates. The country faces challenges like an aging population and a lacking education system, making its growth outlook uncertain.

The BoJ has constraints against raising interest rates due to Japan's massive government debt. If they did raise rates, it would severely impact the country's finances. The BoJ's ongoing asset purchases support Japanese businesses, and there's potential for more subsidies, especially in tech sectors (simulative)

Stock buybacks in Japan hit a record in 2022. The current stock market growth seems driven by government actions, with the BoJ owning a significant portion of Japanese exchange-traded funds (ETFs) and their efforts to get companies to buy back their own stock.

While the US and Europe are pushing companies to innovate due to rising interest rates, Japan's approach is more protective. And most of the recent gains seems to be “artificial” due to buybacks and government intervention rather then innovation and growth. The question then needs to be asked, how sustainable is the rally without a clear indication of underlying growth? Can the buybacks and simulative efforts continue to increase asset prices? And what is foreign investors lose favor of investing in Japan and start to take gains out of a recently strong market?

But Warren Buffett

Berkshire Hathaway said its subsidiary, National Indemnity Company, bought stakes in 5 entrenched trading houses in Japan:

Itochu, Marubeni, Mitsubishi, Mitsui and Sumitomo.

Berkshire Hathaway’s stakes are now around 8-9% in each

The five Japanese companies are some of the biggest trading firms in the country, focusing on a diversified asset basket, long-term investments and strong balance sheets, which is right up Buffett’s street. The companies traditionally hold energy and food imports and finished product exports.

Barron’s estimates the total value of the stakes in all five companies is worth $20 billion, with the stakes being another monster move from the legendary investor as all of the stocks have doubled in value on average.

So, it is too late to get in?

What are his future plans?

It is hard to say, and his investments have already done very well. Maybe they have already reached what he considers fair value. Maybe he thinks there is a lot of room to run. Maybe all the money that follows him is already in. Maybe more to come.

At this point, I feel his involvement (without a new, recent investment) brings more questions then answers.

Game Plan

I am not sure how I want to structure my trade as of now, if at all. I am still doing more research and waiting for price to hold the levels we mentioned.

One possible idea would be a long/short trade where going long the Nikkei and short the SP500. The idea would be the Japan stock market would outpace the US market to the upside, while still leaving some protection if a global recession took ahold.

Another would be to actually invest in individual Japanese equities. That is something I am not familiar with. I would rather make a large, Macro bet then try to pick the needle out of the haystack.

For now I am going to watch it carefully and keep you posted. I am leaning towards the long/short idea but have not done anything yet.

I hope this helps you generate some ideas.

—NS